Key takeaways

- Rising geopolitical tensions and global conflicts have driven up the requirement for more investment in defence and security.

- Many investors have shifted their ESG perspectives on these investments.

- Defence is digitalising and opening up opportunities for managers to invest in tech-driven defence companies that mirror familiar tech assets.

The world is experiencing the highest number of state-based conflicts since 1946, according to The Peace Research Institute Oslo (PRIO).¹

This has prompted governments around the world to prioritise national security and increase defence spending. Global military expenditure reached $2.4 trillion in 2023, a 6.8% annual increase in real terms and the steepest year-on-year rise since 2009.²

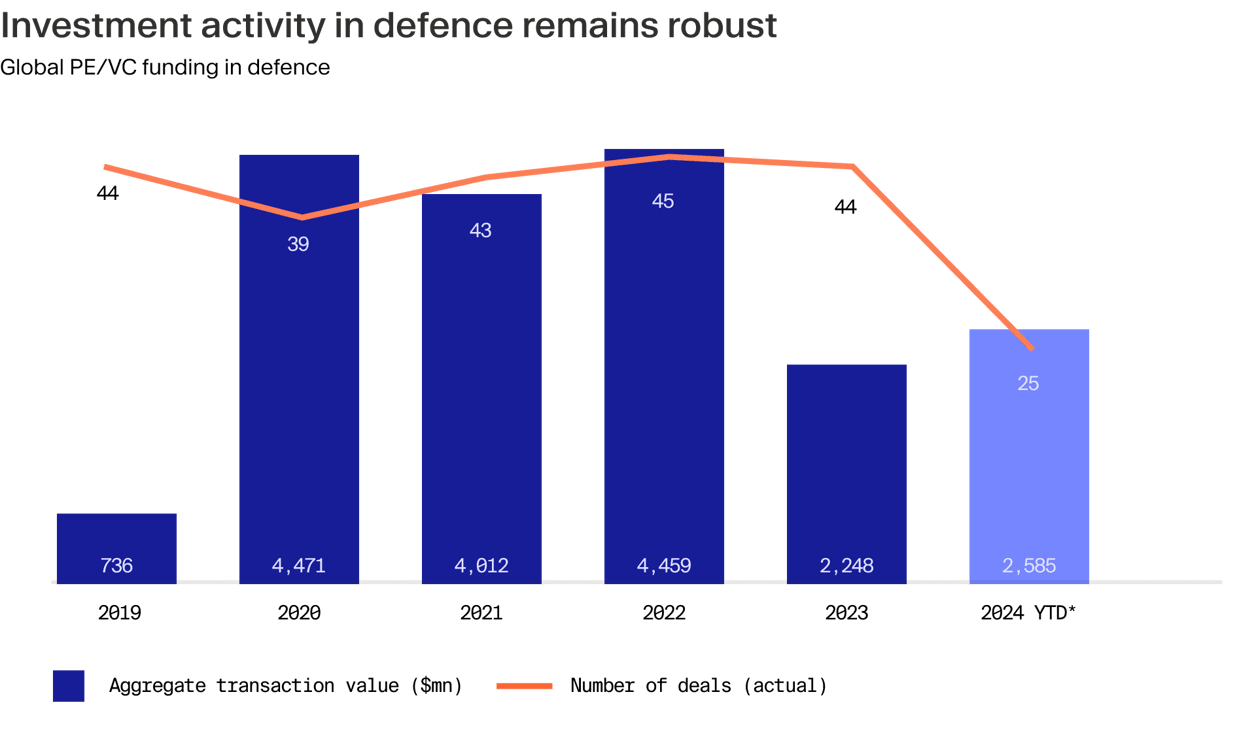

Noting the demand for investment in defence and security, private equity and venture capital firms have moved to increase their exposure in the sector. In 2024 through September, investment totalled $2.6 billion, surpassing the $2.2 billion investment across the entire 2023, according to figures from S&P Global Market Intelligence.³

Concerns and complexity

Aerospace and defence are not new sectors for private markets managers by any means. The Carlyle Group, for example, generated exceptional returns from its investment in defence group QinetiQ in the 2000s,⁴ while Advent International has seen good returns from its 2020 take-private of aerospace and defence group Cobham.⁵

But while some firms have built up impressive track records in the defence space, the sector is complex and difficult to navigate, which has dissuaded managers not familiar with industry from investing, both on commercial and ESG grounds.

The arms industry has raised ethical concerns for investors prioritising ESG and many large institutional investors have had negative screens in place to block investment in weapons and munitions.⁶ Investing in defence also comes with high regulatory and reporting risks. A number of countries, for example, are under arms embargoes and any companies or firms that breach these embargos, inadvertently or otherwise, can face disclosure, investigations and censure by international agencies if breaches are suspected.⁷

In addition to ESG-related concerns, managers have also been reluctant to invest capital in defence for commercial reasons. Barriers to entry are typically high, with government defence contracts dominated by a select group of large players.⁸

There is also a perception that defence companies are capital intensive, hardware-focused businesses that are more difficult to scale⁹ and tend to trade at lower multiples than assets in other sectors.¹⁰

Shifting perspectives

The shifting geopolitical landscape and the increasingly important role of technology and AI in defence strategy and capability, however, are driving a shift in how institutional investors and PE managers are thinking about investments in defence.

Wars in Ukraine and the Middle East and rising tensions in the South China sea and Korean peninsula have highlighted the importance of well-resourced defence infrastructure as a cornerstone of national and economic security.¹¹

Institutions that have had negative defence screens in place previously have shown more flexibility when it comes to investing in the sector,¹² given its crucial role in providing security.

The growing prominence of technology in defence, meanwhile, has reframed the commercial drivers in the sector, opening up further room for managers to put money to work in defence.

Deloitte notes that technology is becoming increasingly important, as cybersecurity, AI unmanned military systems and advanced air mobility capability reconfigure defensive strategy. These developments are not only impacting frontline defence spending, but also investment servicing and maintenance and supply chain optimisation.¹³

The “digitalisation” of defence has opened up opportunities for VC and PE companies to invest in the sector.

Franklin Venture Partners, for example, has invested in Anduril Industries, an autonomous weapons company that combines cheap hardware with AI-powered software to provide drones with military capabilities. The business secured a $1.5 billion funding round in 2024.¹⁴

Andreessen Horowitz has been one of the most active investors in the sector. It was an investor in the Anduril funding round and has also backed ZeroMark, a start-up developing high-end targeting systems,¹⁵ and Saronic, a developer of autonomous surface vessels.¹⁶

Other firms displaying a strong appetite for defence fund rounds have included Founders Fund, 8VC, Alumni Ventures and Silent Ventures, among others.¹⁷

Investors are also seeing opportunities in areas where there are dual-use technologies that are focused on defence, but also have non-defence applications, such as GPS and cybersecurity technology.

These dual-use technologies can be scaled along similar lines to conventional technology assets, such as software-as-a-service (SAAS) companies, that private markets investors are familiar with.¹⁸

Indeed, the evolution of what is classified as a defence business has given managers the confidence to lean into the sector more assertively.

A defence VC boom in Europe

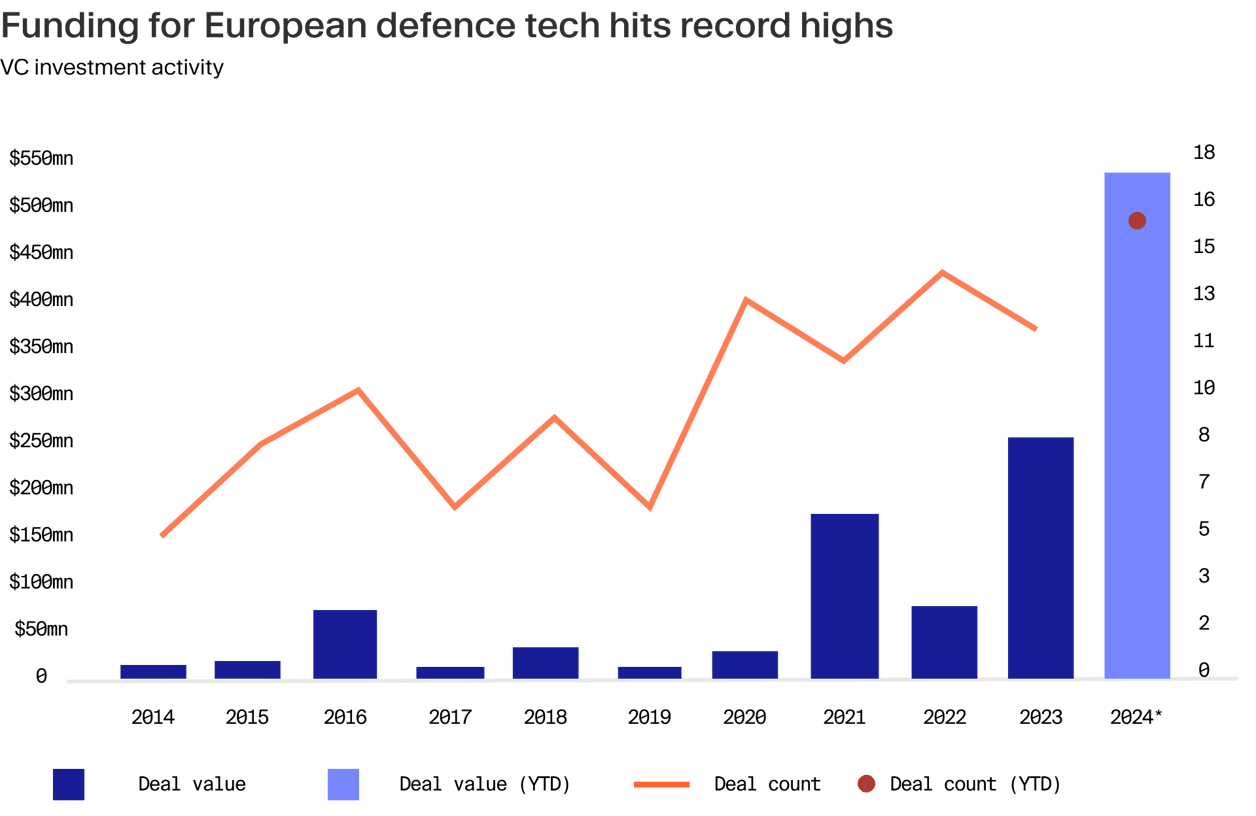

The surge in VC investment in defence has been particularly pronounced in Europe, where Pitchbookfigures show defence tech attracting record levels of investment.¹⁹

Deal value to the middle of October has come in at $532 million, more than double the levels recorded for the whole of 2023, which was the previous record year for investment in the space.²⁰

The specific domain and sector expertise required to succeed in the defence sector, coupled with rising defence budgets, have made defence tech one of the few areas where emerging VC managers have been able to gain traction with investors in what has been an otherwise challenging market for all but the most established VC firms.

D3 Venture Capital, Scalewolf and Twin Track adventures are just some of the new players that have emerged in Europe to invest in defencetech and dual-track defence assets.²¹

The growth in Europe’s defence technology ecosystem has been further buoyed by government initiatives to spur a defence sector that is still significantly smaller than its US counterpart.²²

The EU, for example, has launched a €175 million equity fund to crowd in private sector investment into defence research and development.²³ NATO, meanwhile, has launched a €1 billion NATO Innovation Fund to finance disruptive technologies across the areas of AI, biotechnology, energy and propulsion, manufacturing and space.²⁴

Against this supportive backdrop, a number of start-ups in Europe have secured headline-grabbing funding rounds.

One of the biggest deals in the sector saw Helsing, a German-based company that develops AI software for defence applications, secure a $489 million funding round led by General Catalyst that valued the business at $5.4 billion. According to Crunchbase this is the second-largest defencetech funding round on record.²⁵

Finland’s ICEYE, a developer of synthetic aperture radar (SAR) satellite operations for Earth Observation, is another European start-up with defence capabilities to have successfully tapped investors, raising $93 million in its Series E funding round earlier this year to bring total investment in the business up to $438 million.²⁶

French start-up Unseenlabs, another satellite observation developer, meanwhile, landed an €85 million Series C funding round at the beginning of 2024.²⁷

Long-term growth ahead

The momentum behind private markets investment in defence is expected to continue building as governments increase defence budgets in response to rising geopolitical tensions and the digitalisation of defence lowers barriers to entry.

This enables managers and investors to back solutions that can be scaled and that don’t require the same heavy capital expenditure typical in “traditional” defence businesses producing military hardware.

Finally, we believe that the defence sector is set to attract capital and interest from a growing and more diverse range of managers and investors.

¹ https://www.prio.org/news/3532 ² https://www.sipri.org/media/press-release/2024/global-military-spending-surges-amid-war-rising-tensions-and-insecurity ³ https://www.spglobal.com/marketintelligence/en/news-insights/latest-news-headlines/rise-in-defense-sector-funding-defies-broader-venture-capital-slump-83265012 ⁴ https://www.privateequityinternational.com/carlyle-to-complete-full-exit-from-qinetiq-2/ ⁵ https://www.flightglobal.com/aerospace/latest-cobham-sale-will-take-divestment-proceeds-past-7bn-mark/154081.article ⁶ https://www.rothschildandco.com/en/newsroom/insights/2024/06/rothschild-martin-maurel-investing-in-the-defence-sector/ ⁷ https://www.unpri.org/pri-blog/the-defence-sector-in-focus-common-esg-risks/12689.article ⁸ https://www.spglobal.com/marketintelligence/en/news-insights/latest-news-headlines/rise-in-defense-sector-funding-defies-broader-venture-capital-slump-83265012 ⁹ https://pitchbook.com/news/articles/defense-tech-boom-spawns-wave-of-new-european-gps ¹⁰ https://www.spglobal.com/marketintelligence/en/news-insights/latest-news-headlines/rise-in-defense-sector-funding-defies-broader-venture-capital-slump-83265012 ¹¹ https://www.spglobal.com/marketintelligence/en/news-insights/latest-news-headlines/rise-in-defense-sector-funding-defies-broader-venture-capital-slump-83265012 ¹² https://www.rothschildandco.com/en/newsroom/insights/2024/06/rothschild-martin-maurel-investing-in-the-defence-sector/ ¹³ https://www2.deloitte.com/us/en/insights/industry/aerospace-defense/aerospace-and-defense-industry-outlook.html. ¹⁴ https://www.anduril.com/article/anduril-raises-usd1-5-billion-to-rebuild-the-arsenal-of-democracy/ ¹⁵ https://www.businesswire.com/news/home/20240529043192/en/ZeroMark-Secures-7M-in-Seed-Funding-for-%E2%80%9CHandheld-Iron-Dome%E2%80%9D ¹⁶ https://www.prnewswire.com/news-releases/saronic-raises-175-million-in-series-b-funding-valuing-company-at-1-billion-302201280.html ¹⁷ https://www.astutegroup.com/news/industrial/vcs-march-on-defence-tech-a-2-5-billion-boom/ ¹⁸ https://assets.kpmg.com/content/dam/kpmg/xx/pdf/2021/07/the-private-equity-opportunity-in-defense-web.pdf ¹⁹ https://pitchbook.com/news/articles/defense-tech-boom-spawns-wave-of-new-european-gps ²⁰ https://pitchbook.com/news/articles/defense-tech-boom-spawns-wave-of-new-european-gps ²¹ https://pitchbook.com/news/articles/defense-tech-boom-spawns-wave-of-new-european-gps?sourceType=NEWSLETTER ²² https://pitchbook.com/news/articles/defense-tech-boom-spawns-wave-of-new-european-gps?sourceType=NEWSLETTER ²³ https://sciencebusiness.net/news/dual-use/eu-launches-eu175m-equity-fund-prime-private-investment-defence-rd ²⁴ https://tinyurl.com/vca3juvt ²⁵ https://news.crunchbase.com/ai/defense-tech-helsing-unicorn-anduril/ ²⁶ https://www.iceye.com/press/press-releases/iceye-raises-oversubscribed-growth-funding-round-to-expand-global-sar-leadership ²⁷ https://unseenlabs.space/2024/02/26/unseenlabs-announces-a-record-breaking-fundraising-of-e85-million

- 1 Minimum investment may vary by country and local regulation.

- 2 Source: McKinsey "Private Markets Annual Review 2022"

- 3 Past performance is no guarantee of future returns.