Key takeaways:

- The Federal Reserve's interest rate cut, the first since March 2020, signals a shift towards more favourable conditions for private equity dealmaking and portfolio management.

- Lower interest rates typically lead to cheaper leverage, improved cash flows for portfolio companies, higher valuations and improved exit opportunities.

- While the full effect of lower rates on private equity might take some time to materialise, the positive psychological impact on markets should not be underestimated.

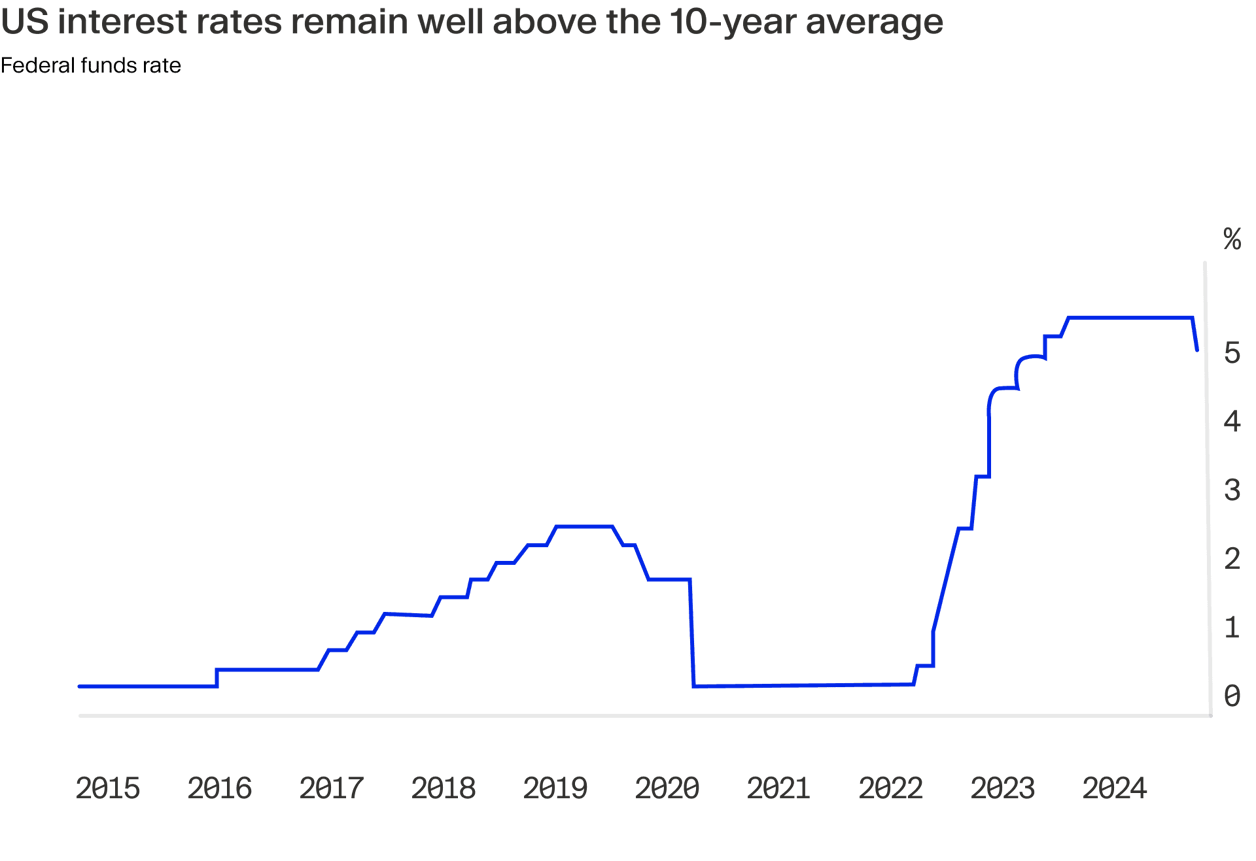

As widely anticipated, the Federal Open Market Committee (FOMC) recently lowered the benchmark federal funds rate by 50 basis points to a target range of 4.75-5%.¹

This is big news because it’s the first rate cut in the US since March 2020, when central banks the world over acted to stimulate economies and financial markets in the immediate aftermath of the COVID crash and ensuing pandemic.

The Fed’s announcement follows a series of rate cuts by other major central banks, including the European Central Bank, which again lowered its deposit rate earlier in September, by 25 basis points to 3.50%.²

With inflation having fallen back to target, the Fed’s attention is now turning to supporting economic stability and the labour market following the fastest pace of rate hikes in the country’s recent history.

How rates work in practice

When central banks lower interest rates, it reduces the cost of borrowing for banks and other financial institutions. This cheaper access to capital generally encourages more borrowing and lending activity in financial markets and the economy, a stimulus for GDP growth.

While clearly positive, investors are cautioned against putting too much store in this latest development. There will be some immediate impact on privately held asset valuations; however, rates will remain elevated. More than anything, it’s a psychological relief and marks a turning point—a step towards greater monetary easing and looser credit conditions.

Rates in a private equity context

Taking a medium-term perspective, we believe the Fed’s decision has significant, positive implications for private assets over the next 12-24 months.

Cheaper, more accessible leverage

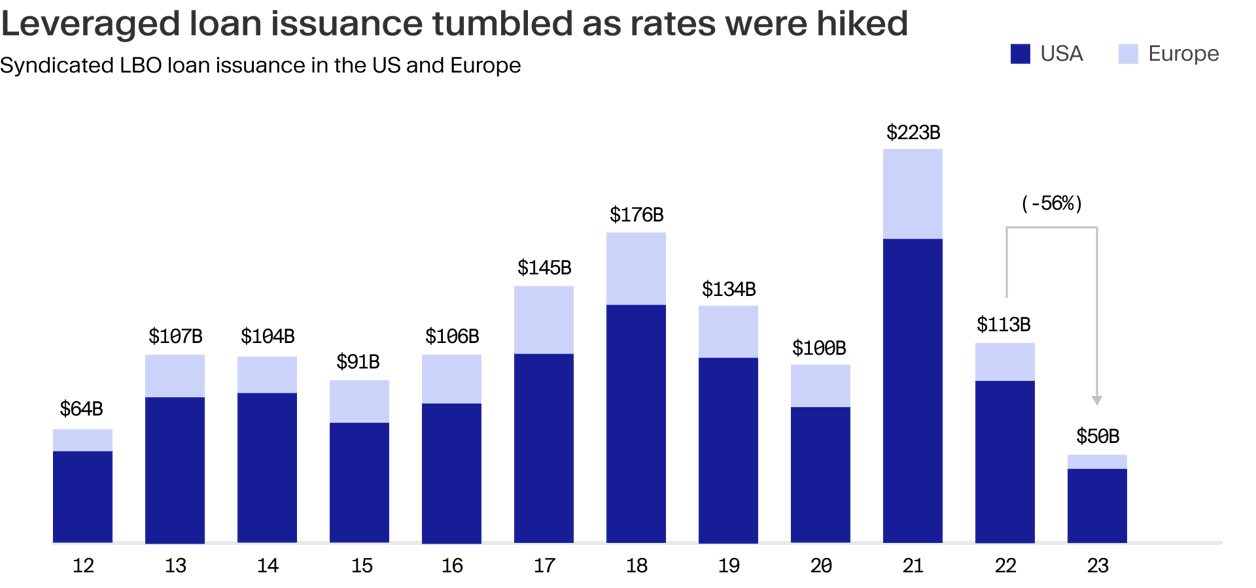

Private equity is often reliant on debt to finance deals. A substantial share of an average buyout fund performance is generated from the application of leverage to target companies’ capital structures. Over the past two years, the higher expense and more restricted access to debt has stifled funds’ ability to execute deals that meet their cost of capital. Naturally, this has seen dealmaking decelerate. In 2023, the value of syndicated LBO loan issuance in the US and Europe cratered by 56% to a decade-plus low of just $50 billion. This followed a similarly steep year-on-year decline of 49% to $113 billion in 2022, from what was admittedly an historic high watermark set in 2021.⁴

LBOs have consequently been made with meaningfully less leverage, which is observed across various metrics. Last year, equity contributions to deals reached 51% for the first time on record. The average debt-to-EBITDA ratio, a measure of the amount of earnings available to pay down debt, fell to just 4.8x from 6.0x a year prior.⁵

The retreat of banks meant that some sponsors went as far as fully financing buyouts with equity and deciding to refinance when conditions permitted. For example, KKR in 2022 chose to acquire French insurance broker April Group initially in an all-equity deal.⁶ Only later, on the deal’s closing, did CVC Credit provide senior facilities to support the buyout.⁷ From here on out, a series of further Fed cuts and subsequently cheaper, more accessible debt is likely to see a sustained rebound in PE dealmaking and normalisation of leverage ratios.

Improved cash flows

Over the past two years, the rise in interest rates has impacted buyout-backed companies' ability to cover their interest expenses. Interest coverage ratios—a measure of a company’s ability to meet interest payments from its cash flows—have fallen sharply.

In the US, the interest coverage ratio for buyout-backed firms has dropped to around 2.4x cash flow, and in Europe, it stands at 2.6x.⁸ These are the lowest levels observed since the global financial crisis (GFC), indicating that many portfolio companies are finding it increasingly challenging to manage their debt burdens. This is compounded by the fact that a significant volume of leveraged loans are coming due in the near term. In 2023 alone, around $95 billion in leveraged loans needed refinancing at higher rates. For PE funds, this presents a challenge, especially if they have not yet executed exits or found alternative means to manage these upcoming liabilities. When interest rates are lowered, the cost of servicing this debt declines, thereby boosting free cash flow available to portfolio companies. This can be crucial for maintaining operations, investing in growth opportunities and supporting debt repayments.

Lower rates would also create a more favourable environment for refinancing existing debts, thereby stabilising interest coverage ratios and allowing for greater financial manoeuvrability.

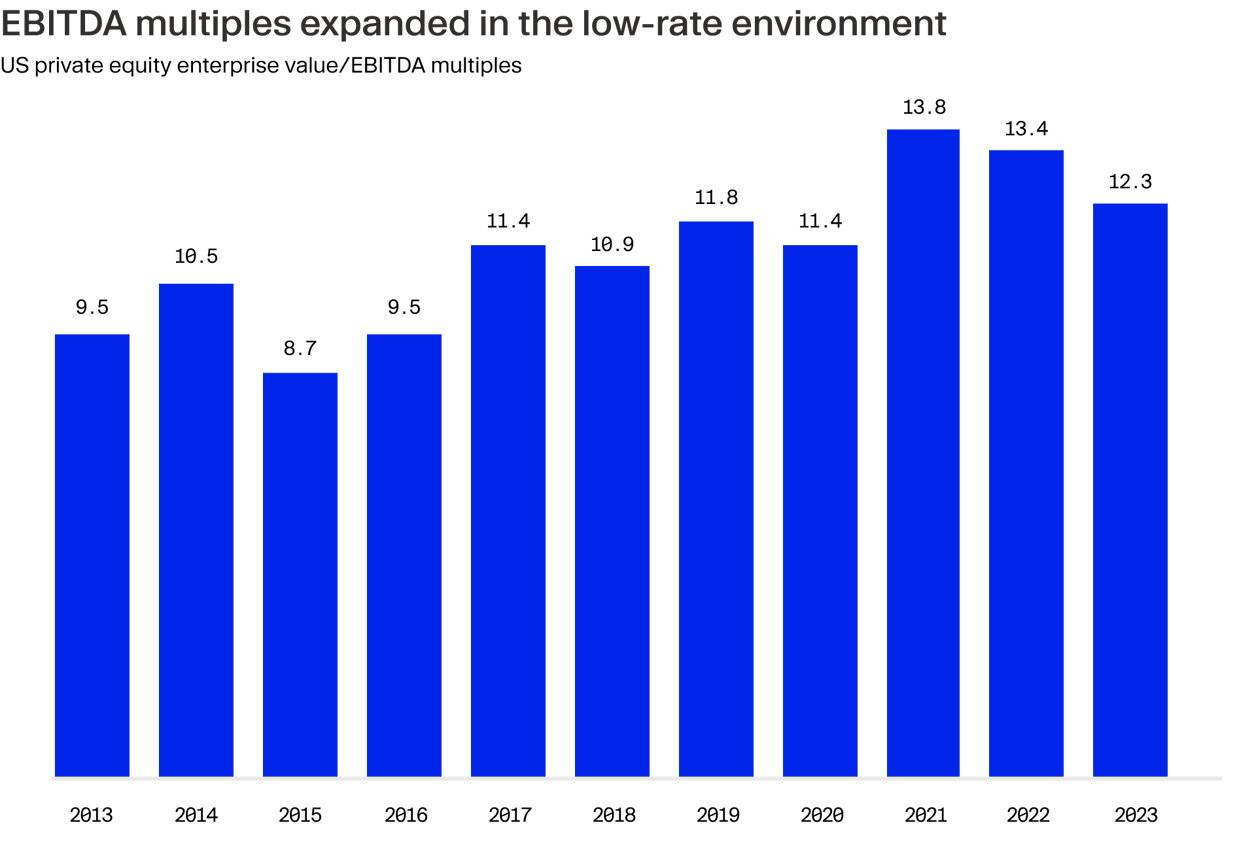

Higher valuations

It’s broadly accepted that interest rates and equity valuations are inversely correlated, in both public and private markets, all else being equal. When interest rates rise, borrowing becomes costlier, reducing leverage capacity and driving down EBITDA multiples as buyers demand lower valuations to offset higher financing costs.

Turning this on its head, lower rates enable PE funds to use more leverage which increases acquisition prices and lifts EBITDA multiples.

This also applies in segments of private markets where leverage generally isn’t applied to deals. Venture capital and growth equity fund managers commonly use discounted cash flow (DCF) models to value startups and growth companies, because in many cases these businesses’ present-day financials are weak or even negative.

A DCF approach estimates the value of a startup based on its expected future cash flows, discounted back to their present value. When interest rates move lower, the discount rate in these models decreases, making future cash flows more valuable in today’s terms, thereby lifting company valuations.⁹ Exit opportunities

Perhaps most importantly, lower interest rates have the potential to reinvigorate exit markets.

With funds holding $3.2 trillion in unsold assets globally, according to Bain¹⁰, there is immense pressure from liquidity-starved LPs to see capital distributions. A more accommodative rate environment can energise public markets, making it easier for large-cap private equity funds to cash out. However, while IPOs capture headlines due to their scale and accessibility to a broader pool of investors, they constitute only 10-15% of global PE exits by volume and value.¹¹ More importantly, lower borrowing costs can reignite secondary buyouts—deals where one private equity firm sells to another. These sponsor-to-sponsor transactions represented nearly one-third of divestments in Q1 2024¹² and are a staple exit route for the industry.

Readier access to debt financing and on more attractive terms can spur new PE acquisitions, in turn increasing exits made by fund managers to their peers. This has the potential to alleviate the distribution bottleneck by allowing capital to flow more freely back to LPs.

Final thoughts

The Fed’s rate cut is a pivotal moment after two years of aggressive tightening. Further easing should bulwark economic growth and stabilise markets. The dot plot suggests rates may remain elevated relative to historic lows, signalling the zero-interest rate policy era is likely a thing of the past.

Prior to this week’s FOMC, markets expected the Fed to deliver 75-100 basis points of cuts through the remainder of the year, and the central bank is anticipated to reach a neutral rate of 3.0-3.25% by mid-2025.¹³¹⁴

Numerous variables including GDP growth, gross domestic income (GDI) growth, credit defaults and bankruptcies, consumer spending and the unemployment rate will continue to be closely monitored by markets for signals of strength in the US economy.

Rates are just one piece of the puzzle. For private equity, though, the path to lower rates is a welcome stimulus: cheaper debt, improved cash flows, improved valuations and better exit prospects are essential ingredients for potentiating realised returns and meeting LP expectations.

¹ https://www.ft.com/content/bff9e6d8-8906-4b3d-9ff3-72b091b6cd9e ² https://www.reuters.com/markets/rates-bonds/ecb-cut-interest-rates-growth-dwindles-outlook-unclear-2024-09-11/ ³ https://www.ft.com/content/bff9e6d8-8906-4b3d-9ff3-72b091b6cd9e ⁴ https://www.bain.com/insights/private-equity-outlook-liquidity-imperative-global-private-equity-report-2024 ⁵ https://pitchbook.com/news/articles/lbo-report-sponsor-equity-contributions-top-50-yields-soar-as-deal-financing-costs-remain-high ⁶ https://www.bloomberg.com/news/articles/2022-12-01/kkr-used-equity-rather-than-debt-to-fund-buyout-of-april-group ⁷ https://www.cvc.com/media/news/2023/2023-04-11-cvc-credit-supports-kkr-s-acquisition-of-april-group/ ⁸ https://www.bain.com/insights/private-equity-outlook-liquidity-imperative-global-private-equity-report-2024 ⁹ https://www.statista.com/statistics/892488/enterprise-value-to-ebitda-in-europe-the-middle-east-and-africa-by-sector ¹⁰ https://www.bain.com/insights/private-equity-outlook-liquidity-imperative-global-private-equity-report-2024 ¹¹ https://www.mckinsey.com/industries/private-capital/our-insights/mckinseys-private-markets-annual-review ¹² https://pitchbook.com/news/articles/private-equity-uptick-secondary-buyouts ¹³ https://www.reuters.com/markets/rates-bonds/fed-deliver-three-25-quarter-point-rate-cuts-this-year-recession-unlikely-2024-08-19/ ¹⁴ https://think.ing.com/articles/federal-reserve-scenarios-more-twists-and-turns-to-come

- 1 Minimum investment may vary by country and local regulation.

- 2 Source: McKinsey "Private Markets Annual Review 2022"

- 3 Past performance is no guarantee of future returns.