Key takeaways:

- Consolidation in private markets is accelerating, with large, diversified GPs acquiring smaller firms to build scale and expand into new asset classes.

- Investor preferences are shifting toward established managers who can offer a broader range of strategies and greater stability, making it harder for smaller, independent firms to compete.

- A more concentrated market has mixed implications for investors, offering stability and reducing the administrative burden of managing multiple relationships, while potentially reducing choice and competition.

Private markets are undergoing a tectonic shift. In the first half of 2024, there has been a surge of acquisitions targeting GPs themselves as industry giants expand their empires, taking over smaller firms.

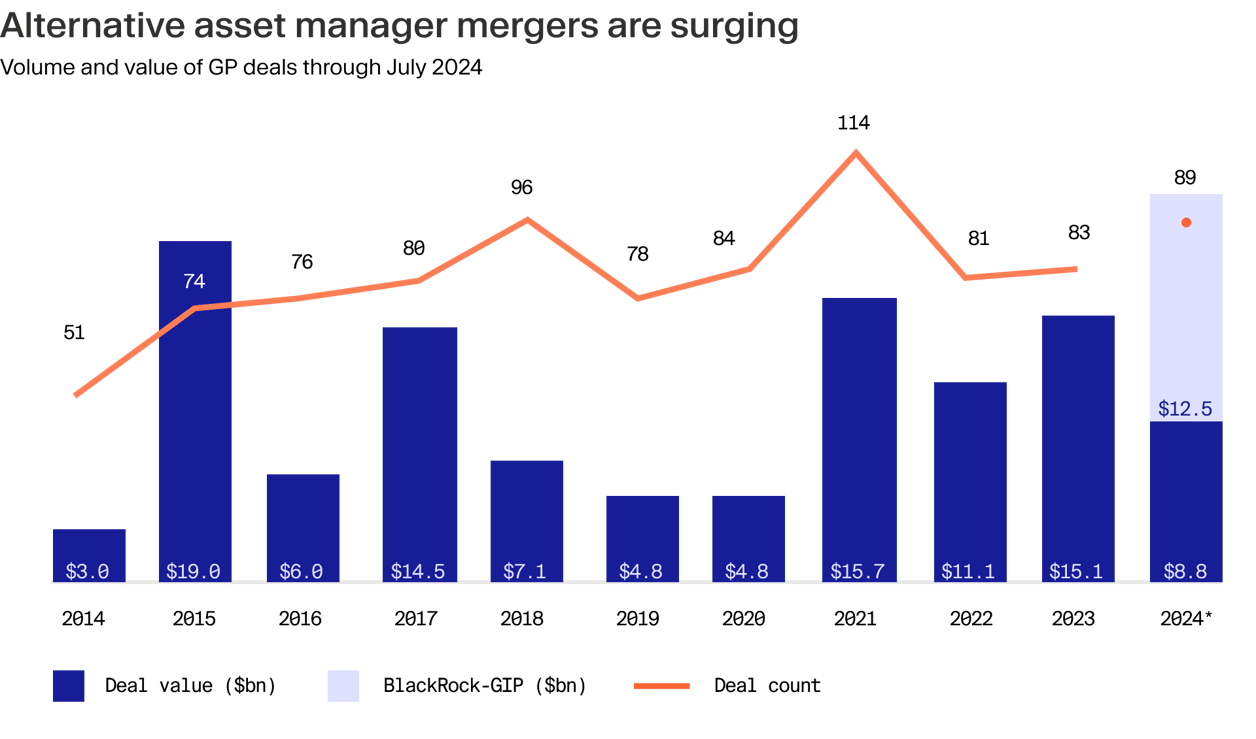

Recent examples include Clearlake Capital's acquisition of pan-European private debt specialist MV Credit in September¹ and BlackRock's hefty $12.5 billion purchase of Global Infrastructure Partners in January.²

The bigger picture

This wave of consolidation is neither a passing trend nor exclusive to private markets. The broader asset and wealth management industry is in the midst of an accelerating evolution. Projections suggest that by 2027, consolidation or extinction could touch 16% of existing asset managers — double the historical turnover rate.³ Adaptability and scale are becoming prerequisites for survival. Increasing regulatory oversight and compliance costs are making it challenging for smaller firms to operate independently, pushing them to merge with larger entities that can better absorb these expenses.

The need for significant investments in technology and the pursuit of economies of scale to counter fee compression are also driving firms to consolidate in order to remain competitive and meet rising investor demands.

GP deals surging

Historically, merging private firms was a complex endeavour fraught with challenges — from blending corporate cultures to aligning compensation structures. These hurdles prevented consolidation activity from gaining meaningful ground. However, public listings have armed larger GPs with fresh funding avenues, enabling them to pursue strategic acquisitions more aggressively. In one of the largest IPOs in Europe this year, private equity house CVC Capital Partners raised €2 billion and now trades on the Euronext Amsterdam with a market cap of around €20bn.⁴

Following the float, the firm completed its acquisition of an initial 60% stake in infrastructure platform DIF Capital Partners,⁵ as well as securing an outstanding 20% stake in secondaries firm Glendower Capital that it initially built a majority position in three years prior. The numbers tell the story here: this year is on track to set a record for GP acquisitions, surpassing previous highs from 2021 and 2015. In 2024 through July alone, GPs completed 84% more acquisitions of their peers compared with the same period last year, with both control and minority deals seeing dramatic increases, according to Pitchbook.⁶

Forces fuelling consolidation

There are numerous reasons why the industry is in the grip of a consolidation wave.

Shift to large managers

In times of market uncertainty, investors gravitate towards stability and familiarity. This preference has led them to favour large, diversified firms with established track records that can cater to all of their asset class needs over more piecemeal approaches using smaller, niche players.

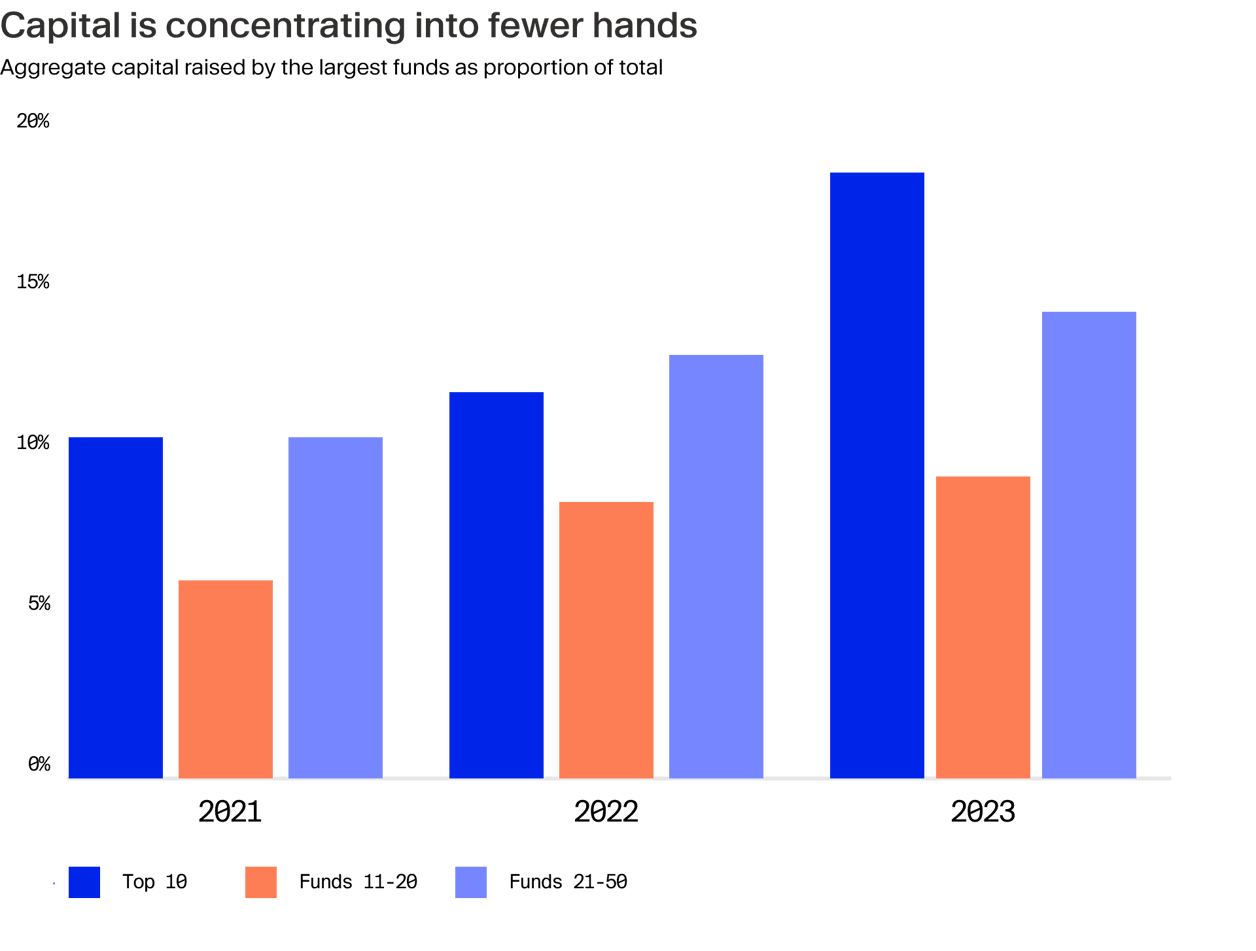

Fundraising has become particularly challenging for smaller private equity managers. Astonishingly, the 10 largest funds captured 18% of all capital allocated by investors in 2023, nearly double their 10% share of fundraising just two years prior.⁷

The top 50 funds, meanwhile, netted around 40% between them. Investors are placing greater confidence in established firms, believing they are better equipped to manage market pressures and deliver consistent returns.

Debt pressures from the low-rate era

The era of low-interest rates encouraged many PE managers to take on debt on favourable terms. However, the recent interest rate adjustment cycle has made refinancing these obligations a significant burden. Smaller firms, in particular, are feeling the squeeze as they struggle to manage the increased cost of debt. Many of these firms, unable to secure affordable refinancing, are facing difficult choices. While some may hope for strategic buyouts, the likely outcome for many will be a wind-down or transition into run-off mode, eventually disappearing from the industry altogether. This shakeout will lead to fewer players overall, leaving the field increasingly dominated by larger, more resilient firms that can withstand this refinancing cycle.

Compliance costs under heightened scrutiny

The regulatory landscape has become more demanding, adding layers of complexity and cost. Compliance requirements, once manageable, now represent a substantial financial burden, especially for smaller firms with limited resources. For example, before being vacated in June by three-judge panel of the US Court of Appeals for the Fifth Circuit, the SEC's recent Private Fund Adviser Rule mandated increased transparency in fees, expenses and conflicts of interest.

Similarly, new ESG disclosure standards under the EU’s Sustainable Finance Disclosure Regulation (SFDR) require private equity firms to substantiate and document their sustainability claims, which often necessitates specialised expertise and resources. Integrating regulatory demands across lean teams is challenging. Given the choice, smaller firms may find it more practical to merge with larger platforms that can absorb and distribute these expenses more effectively.

Inorganic growth through strategic acquisitions

For large GPs, acquisitions offer a strategic shortcut to diversify into adjacent, highly complementary asset classes. Entering markets like private credit, secondaries, infrastructure and real estate organically is time-consuming and fraught with uncertainty. Acquisitions present a more efficient pathway to achieving the same goals. Since 2012, a significant 60% of acquisitions by major firms have targeted related asset classes.⁸ Franklin Templeton's purchase of Lexington Partners for $1.75 billion in 2021 is a prime example, marking a synergistic expansion into the booming secondary market space.⁹

Similarly, buyout firm Clearlake’s recent purchase of MV gave it a presence in the fast-growing private credit segment.¹⁰

Implications for investors

It would be simple if consolidation was all upside, but alongside the potential benefits investors have their concerns. While larger firms may offer stability and a broader array of services with one relationship, many limited partners (LPs) are approaching this trend with a degree of scepticism. These apprehensions centre on three main areas:

1. Loss of independence

LPs value the specialised and nimble approach that independent managers provide. There are concerns that, as firms become absorbed into larger entities, this agility may be lost. Bureaucracy could stifle innovation, and unique investment strategies might be de-prioritised in favour of a more standardised approach. This bloating effect may not align as closely with investors’ interests.

2. Succession and continuity

Stability in management and strategy can be a deciding factor for LPs when selecting GPs. Consolidation can disrupt this stability, raising questions about succession planning and the continuity of investment approaches under a new GP franchise. This can be reason enough for long-term investors with a firm to terminate the relationship and seek alternatives.

3. Reduced competition and choice

A market dominated by fewer, larger firms could ultimately inhibit competition, limiting options for investors. There's a concern that this could result in a homogenised market with less strategy innovation. With fewer options available to LPs, dominant GPs might also have more leverage in prioritising income over client-specific needs as scale becomes the primary objective.

What's next?

There’s no end in sight to today’s industry mergers. Consider that a low-ball estimate puts the total number of PE firms globally at 10,000, a number that will almost certainly fall over the next decade as the industry consolidates into fewer, larger players.¹¹ Some believe this figure could even lose two zeros over the next decade, as just 100 mega managers emerge.¹² The rise of larger, well-resourced firms offers clear advantages, including stability, a wider range of strategies per manager relationship and potentially better risk management.

However, LPs are vigilant to this ongoing transformation. Alignment of interests, maintaining a diversity of choice and staying attentive to changes in fee structures are all critical considerations. It is also the middle that is most likely to feel the squeeze. Smaller, more specialised firms focused on specific sub-sectors or geographies can still thrive by offering unique value propositions and generating alpha in less saturated markets.

These firms can continue capitalising on opportunities that are overlooked by larger entities with higher deal thresholds. We believe that these niche firms will maintain their relevance and success through differentiation.

Spotlight: Distinguishing GP stakes investing from strategic mergers

GP stakes investing has emerged as a notable alternative investment strategy in private markets, but should not be confused with manager deals.

Strategic mergers are purely that—strategic. In these transactions, the acquiring firm invests its own capital, not funds from its investors, to purchase another firm outright. The primary goal is to expand private market strategies and grow fee-generating assets under management (AUM). This approach is about operational integration, adding new capabilities and improving the firm's overall market position.

In contrast, GP stakes investing is conducted through dedicated funds and represents an investment strategy or asset class in its own right. Firms purchase minority shares in a GP to benefit from earnings without seeking control or merger integration, essentially treating the firm like a portfolio company.

This method allows investors to capture growth and share in profits while the GP maintains operational independence. Although GP stakes accounted for just 18% of total deal activity targeting alternative asset managers in 2024 through July, it is an increasingly popular investment strategy.¹³

¹ https://www.mvcredit.com/news/clearlake-acquire-mv-credit ² https://www.blackrock.com/corporate/newsroom/press-releases/article/corporate-one/press-releases/blackRock-agrees-to-acquire-global-infrastructure-partners ³ https://www.pwc.com/gx/en/industries/entertainment-media/outlook/downloads/pwc-awm-revolution-2023.pdf ⁴ https://www.bloomberg.com/news/articles/2024-04-26/cvc-capital-backers-raise-2-billion-in-long-awaited-listing ⁵ https://www.cvcdif.com/news-insights/completion-of-acquisition-dif-capital-partners-by-cvc ⁶ https://files.pitchbook.com/website/files/pdf/Q2_2024_US_Public_PE_and_GP_Deal_Roundup.pdf ⁷ https://www.preqin.com/insights/research/factsheets/fundraising-in-review-the-big-got-bigger-the-smaller-struggled ⁸ https://www.bain.com/insights/is-strategic-m-and-a-finally-catching-on-in-private-capital/ ⁹ https://www.lexingtonpartners.com/press-releases/franklin-templeton-to-acquire-lexington-partners ¹⁰ https://www.morganstanley.com/ideas/private-credit-outlook-considerations#F1 ¹¹ https://hbr.org/2022/07/private-equity-should-take-the-lead-in-sustainability ¹² https://www.ft.com/content/e5372801-4ac6-48f2-876f-656c50e7c069

¹³ https://files.pitchbook.com/website/files/pdf/Q2_2024_US_Public_PE_and_GP_Deal_Roundup.pdf

- 1 Minimum investment may vary by country and local regulation.

- 2 Source: McKinsey "Private Markets Annual Review 2022"

- 3 Past performance is no guarantee of future returns.